Introduction

Large Main Street Bank, a large financial service firm, offers a PCL product. Currently around 40,000 PCL accounts are active, and an average of 65 PCL accounts are opened per day and 25 PCL accounts are closed per day. Currently, Large Main Street Bank requires financial advisors to document why PCL accounts are opened, but they do not require financial advisors to document why PCL accounts are closed. For this reason, Large Main Street Bank does not know why PCL accounts are closed and are essentially flying blind when it comes to deciding how they might improve the PCL product. Large Main Street Bank’s research goal was to collect rich qualitative data and generate a theory about why clients and Financial Advisors are closing their PCL accounts which might be tested at a later time with a large-scale quantitative study.

I chose to contract and work on this project because, as a researcher, I want Large Main Street Bank to better understand their clients and employees lived experiences so their business decisions are grounded in a deep understanding of the role the PCL product plays within people’s lived experiences.

Research Questions

As with most research studies, this one began with a clearly-articulated set of research questions. We set out to identify the following about the PCL product:

Why do Financial Advisors and clients close PCL accounts?

How do collateral account restrictions factor into the decision to close accounts?How do clients express their reasons for choosing to close PCL accounts?

When it comes to PCL, what are the shortcomings?

Methods and Sample Description

I employed a (1) literature review, (2) screener survey, (3) phone interviews, and (4) content analysis for this research study.

Literature Review

I searched for past research studies on the PCL product but could not find any. I widened my search and was able to collect and review two existing research studies related to how consumers approach lending and the values consumers place on personal lines of credit (PLOC) and personal loans (PLOAN).

Content Analysis

I performed a content analysis to examine if and how the existing materials are playing a role in why financial advisors and their clients are closing PCL accounts. I selected six documents based on what would be given to client when opening a PCL, what materials would be given to clients upon closing of a PCL, and what documents Financial Advisors would easily access if they needed information about PCL.

Screener Survey

I performed a screener survey to answer a handful of the businesses’ closed-ended questions. I sent twenty-three recruiting emails and screened seven financial advisors. I employed a purposive and stratified sample of Financial Advisors who are enrolled in the company’s internal research-focused Ambassador Program, had at least five clients close their PCL accounts between 1/9/2019-1/9/2020, have knowledge on reasons those clients closed the PCL accounts, and are comfortable sharing those stories. Seven financial advisors were called by phone and screened. The below questions were asked:

- Are you comfortable sharing stories and reasons why your clients closed their PCL accounts? (Y, N)

- If yes, what are the typical reasons your clients closed their PCL accounts? (open-ended)

- Did any of your clients that closed PCL accounts also have brokerage cash solutions (previously known as command accounts)? (Y,N)

- If yes, how frequently did the restriction on brokerage cash solutions, i.e. command accounts, play a role within the client’s decision to close their PCL account? (almost always, to a considerable degree, occasionally, seldom)

Semi-structured Phone Interviews

Five financial advisors were scheduled for interviews but only four participated in interviews. Each participant was asked a set of standard questions and then questioned further with ad hoc questions based upon where the participant led the conversation. The below questions were asked during the interview. We collected answers from all four financial advisors for the following questions:

Five financial advisors were scheduled for interviews but only four participated in interviews. Each participant was asked a set of standard questions and then questioned further with ad hoc questions based upon where the participant led the conversation. The below questions were asked during the interview. We collected answers from all four financial advisors for the following questions:

- Talk to us about these accounts that closed over the past year. Share the stories of these clients. What led these clients to open and close their PCL accounts?

- How/when did clients decide? What was the process like? How did it work? Did you tell clients to close it? Did clients tell you? Something else?

-Based on your knowledge and experience, why do clients typically choose to close their PCL accounts? Why do clients typically choose to keep their PCL accounts open? Are there any other reasons which are atypical or anomalies?

- Are collateral account restrictions a factor into the decision to close their PCL accounts? If so, how? What other things factor into the decision to close?

- What role do PCL accounts play in your client’s lives?

- Hit: What you love about the PCL product? What is working well?'

- Miss: Where is the PCL product/marketing/etc. falling short?

- Wish: What do you really wish the PCL product could do/offer?

Research Participants

Participant 1 is a male financial advisor located in a city 51 miles northwest of Chicago, IL. He closed 8 PCLs in the past year.

Participant 2 is a male financial advisor located in a city 220 miles southwest of Wichita, KS. He closed 10 PCLs in the past year.

Participant 3 is a male financial advisor located in Palo Alto, CA. He closed 8 PCLs in the past year.

Participant 4 is a male financial advisor located in Canfield, OH. He closed 6 PCLs in the past year.

I faced many limitations during this study.

(1) This was a low budget study, so I conducted remote phone interviews. I was limited in what we could observe using the phone format.

(2) We do not have a transcription service and our research team is busy, so for each interview I had a different person taking notes. This limitation meant I had to listen to each interview again in order to clean up and fill in missing portions.

(3) I experienced a lower than usual response and participation rate because Financial Advisors were extremely busy taking care of their clients during an irregular amount of market volatility. This meant I had to transition to a convenience sample. Two financial advisors I screened were too busy to participate in a 45-minuute interview, and another financial advisor had to cancel at the time of the interview because client needs were a high priority that morning. Because of our low participation rate, we were unable to meet our recruiting goal of 6-10 financial advisors and determined that the project would be put on hold and resumed once the market calmed down.

Assumptions I brought to my research include the thoughts that

(1) clients are self-aware and are capable and willing to self-report both their internal thought process and the external factors that were at play and pivotal to them closing their PCL account to their Financial Advisors;

(2) Financial Advisors are aware and capable of reporting not only their internal thought process and the external factors that were at play and pivotal to clients closing their PCL account but also aware and capable of reporting their clients; and

(3) Financial Advisors have worked with enough clients long enough that they are aware of typical reasons why their clients close PCL accounts.

Analysis

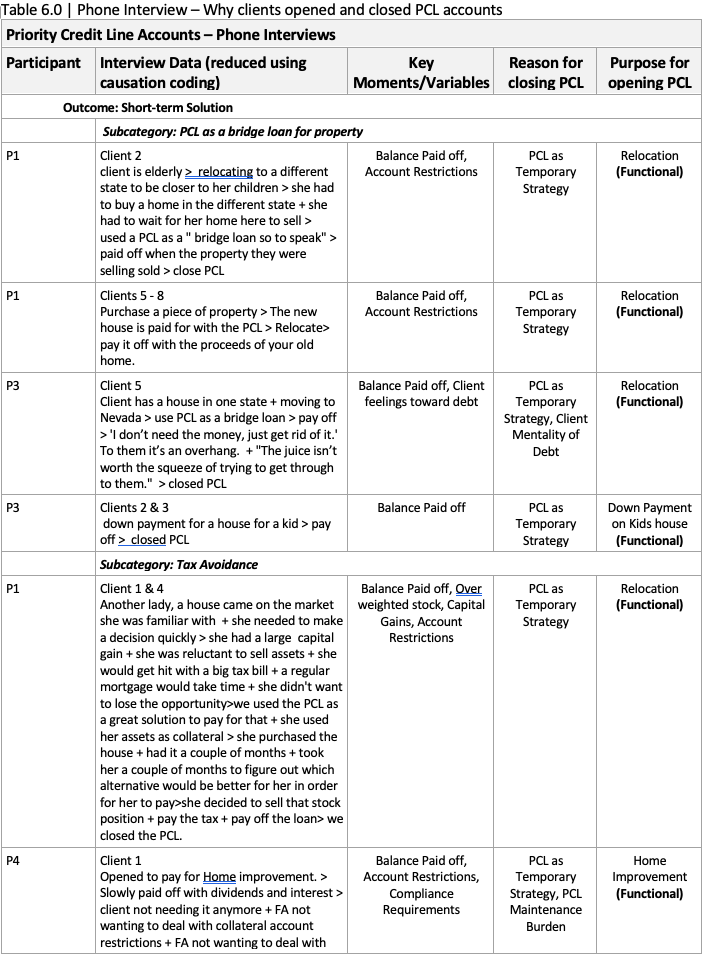

I interviewed four financial advisors and asked them to tell us why they and their clients closed 6-10 PCL accounts between 1/9/2019-1/9/2020. After the interviews, I took the transcripts and formatted their answers in Table 6.0. I reduced their responses using causation coding and created columns where I labeled the interview participant, the clients, the condensed story, the purpose of opening the PCL, the reasons for closing the PCL, and the key motivators/variables that contributed to the decision to close.

I interviewed four financial advisors and asked them to tell us why they and their clients closed 6-10 PCL accounts between 1/9/2019-1/9/2020. After the interviews, I took the transcripts and formatted their answers in Table 6.0. I reduced their responses using causation coding and created columns where I labeled the interview participant, the clients, the condensed story, the purpose of opening the PCL, the reasons for closing the PCL, and the key motivators/variables that contributed to the decision to close.